Celsius ($CELH) - Deep Dive

A deeper look at one of the top consumer goods in the energy drink industry

1. Company Overview & Investment Thesis

Celsius Holdings (NASDAQ: $CELH) is a functional beverage company best known for its flagship CELSIUS energy drink line. Founded in 2004, the company has transformed from a niche fitness-oriented player into a scaled multi-brand “Modern Energy” platform.

Core products emphasizes a “better-for-you” product: zero-sugar, clinically studied ingredients (e.g., MetaPlus formula for metabolism support), vitamins, and natural caffeine — targeted at active, health-conscious consumers rather than traditional high-sugar energy drinks.

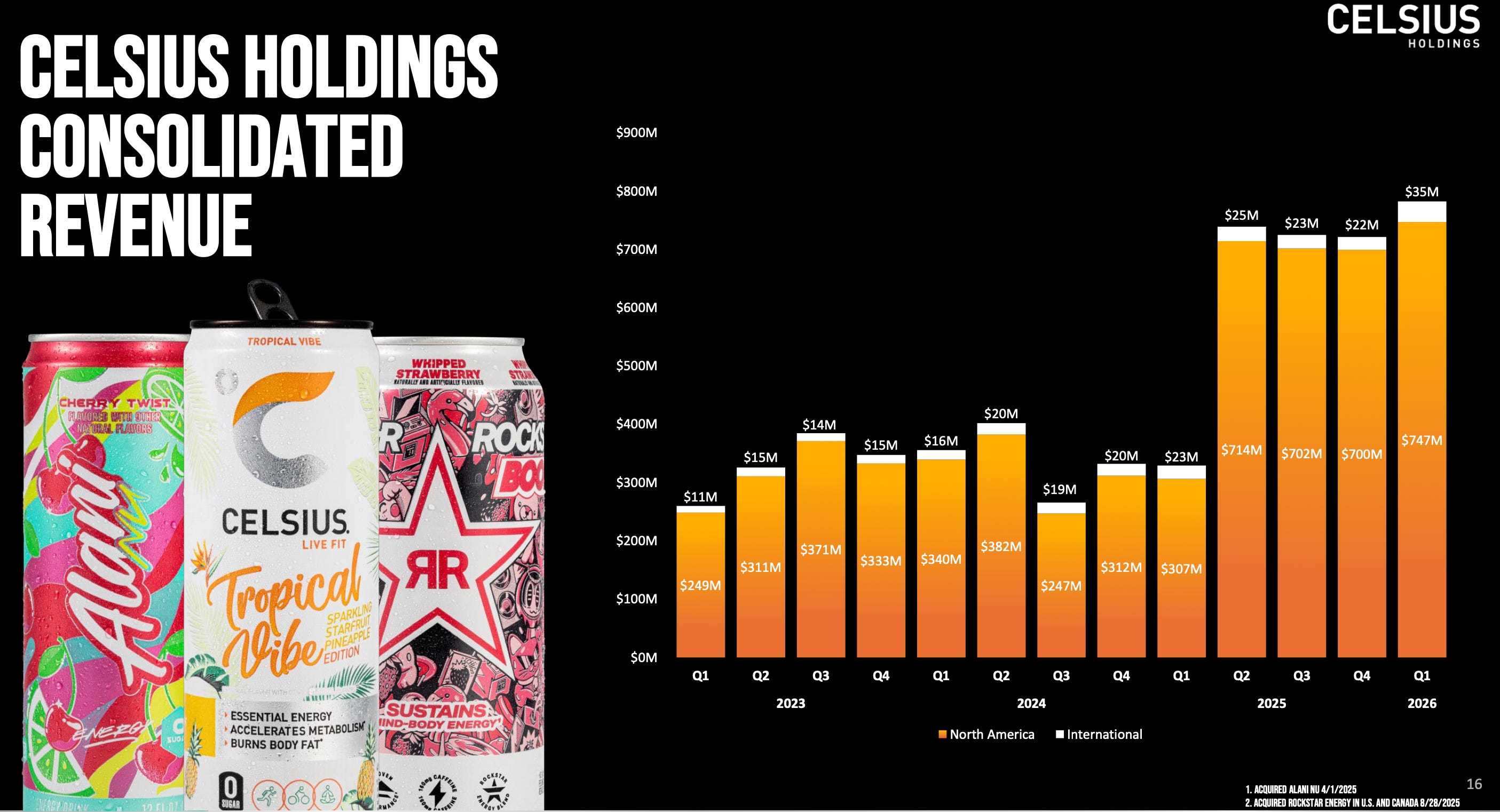

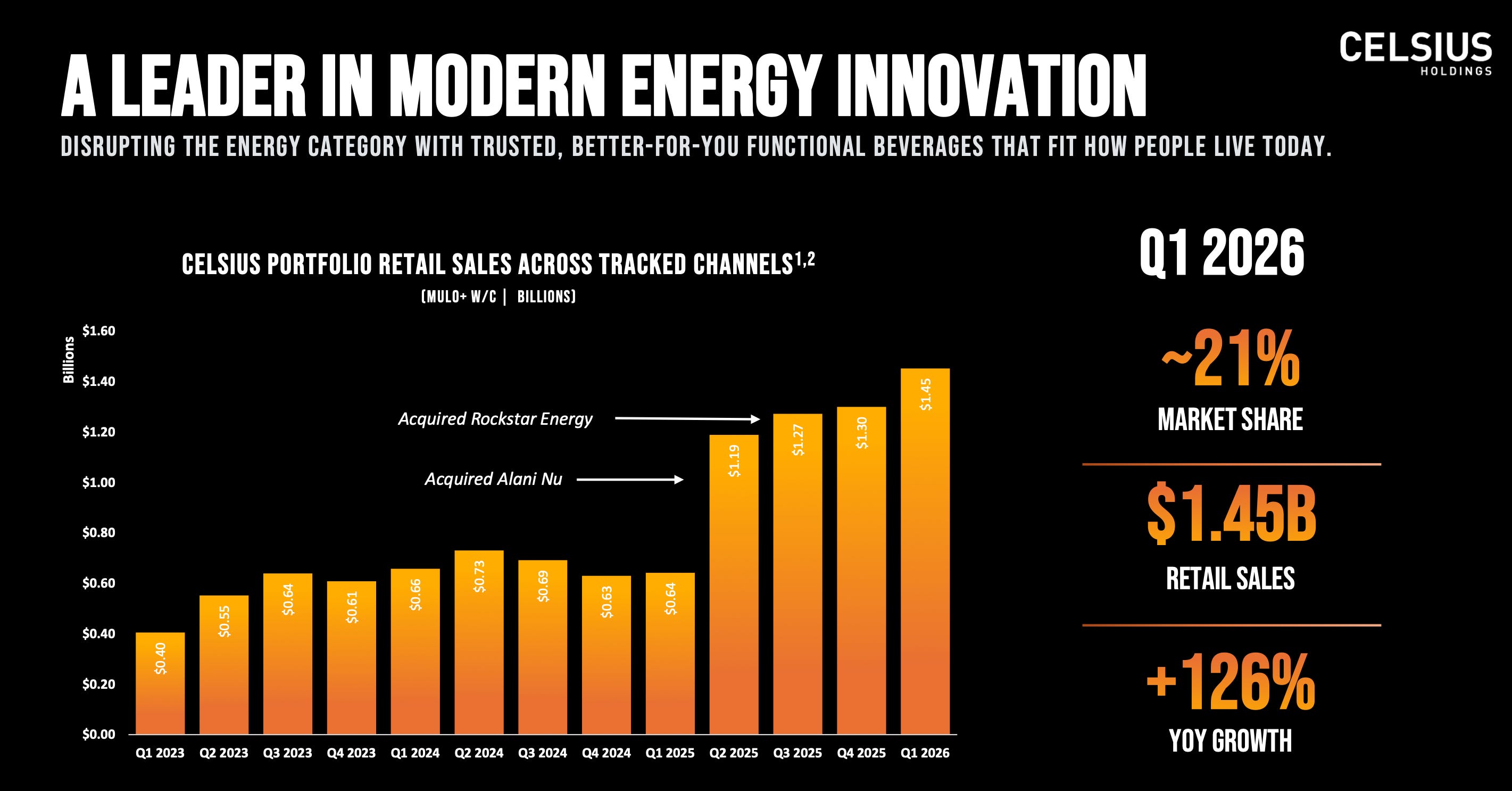

In 2025, CELH accelerated its evolution through acquisitions (Alani Nu in April and Rockstar Energy rights in the U.S./Canada in August), building a portfolio that spans fitness, wellness, and broader energy occasions. The company partners with PepsiCo ($PEP) for distribution in key markets, giving it access to massive retail and convenience channels.

Investment Thesis: Celsius is riding the cultural shift toward healthier, functional beverages in the high-growth energy drink category. With ~20% U.S. market share across its portfolio, strong brand momentum in fitness/wellness, and PepsiCo’s distribution advantage, CELH has scale and execution advantages that smaller players lack. International expansion and portfolio synergies offer further runway and strong growth outlooks. However, it faces intense competition from Red Bull, Monster, and now Costco’s Kirkland energy drink that was recently launched , plus integration risks from recent deals. For retail investors, CELH represents a high-growth CPG story where brand velocity and its distribution moat, thanks to PepsiCo, could drive sustained market share gains — if execution holds.

As of early 2026, the company reported ~$2.5 billion in 2025 revenue (strong growth) and is entering 2026 with improved operating clarity.

2. Industry & Macro Context

The global energy drink market is one of the fastest-growing segments in beverages, driven by demand for convenient energy, focus, and wellness. Side note, multiple studies and surveys confirm that younger generations—especially Gen Z (born ~1997–2012) and younger Millennials—are drinking significantly less alcohol than previous generations did at the same age. They’re also showing stronger health and wellness orientations, with trends toward fitness, mental health awareness, and mindful consumption. Key trends include:

Health-Conscious Shift: Consumers are moving away from high-sugar drinks toward zero-sugar, functional options with added vitamins, nootropics, or metabolism benefits — exactly Celsius’ sweet spot.

Category Growth: Energy drinks have outperformed the broader non-alcoholic beverage industry, with U.S. dollar share gains and expanding occasions (pre-workout, daily focus, social).

Distribution Evolution: Major players like PepsiCo and Coca-Cola are consolidating routes-to-market, favoring scaled brands with portfolio breadth.

Macro Tailwinds: Rising fitness participation, e-commerce, and younger demographics (Gen Z/Millennials) favoring “better-for-you” products. International markets (Europe, Asia) remain underpenetrated.

Headwinds include intense competition (Red Bull ~36%, Monster ~27%, Celsius portfolio ~20% in the U.S.), private-label pressure (e.g., Costco Kirkland), input cost volatility (aluminum, ingredients), and potential category saturation in North America.

Celsius benefits from these dynamics through its functional positioning and PepsiCo partnership, but must continue innovating (flavors, LTOs) and expanding channels to sustain velocity.

3. Business Model, Assets & Competitive Moats

Celsius operates an asset-light model focused on brand, formulation, and distribution. Revenue comes primarily from selling ready-to-drink beverages and related products through retail, convenience, club, and e-commerce channels.

Key Assets:

Strong brand portfolio (CELSIUS, Alani Nu, Rockstar).

PepsiCo distribution network for scale.

Innovation pipeline (new flavors and limited editions).

Competitive Moats:

Brand Equity: “Better-for-you” positioning and clinical claims build loyalty in the fitness/wellness segment.

Distribution Scale: PepsiCo partnership provides broad reach and merchandising priority.

Portfolio Breadth: Multiple brands target different consumers and occasions, increasing shelf space and reducing risk.

Velocity Flywheel: High sell-through rates lead to more retailer support and shelf expansion.

The moat is centered on brand + distribution in a competitive but growing category. It’s narrower than in infrastructure businesses but meaningful for a CPG player. International expansion adds long-term optionality.

4. Management, Governance & Capital Allocation

Celsius is led by a seasoned team with strong CPG and beverage experience. John Fieldly (Chairman and CEO) has guided the company’s growth and multi-brand pivot. The leadership includes executives focused on marketing, supply chain, sales, and finance.

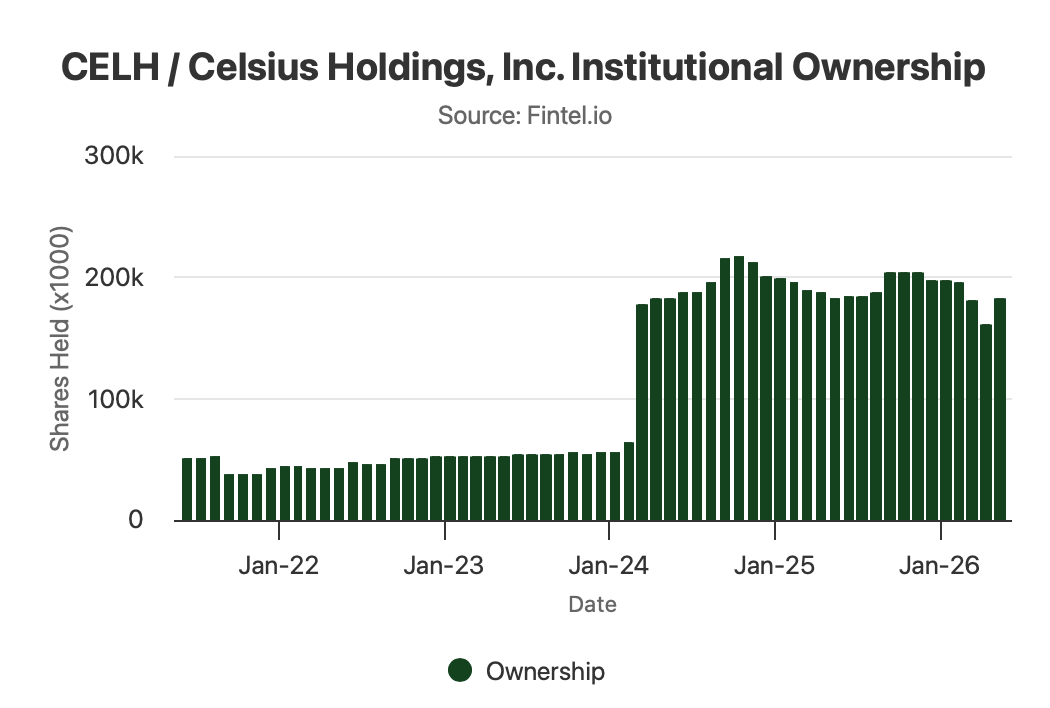

Alignment & Governance: Insider ownership helps align interests. The board includes independent directors with relevant consumer and operations expertise. Governance follows standard public-company standards, with compensation tied to revenue growth, market share, and profitability.

Capital Allocation: Management has used capital for strategic acquisitions (Alani Nu, Rockstar) to broaden the portfolio, marketing to drive awareness, and distribution optimization. Share buybacks have been deployed opportunistically. The shift from pure growth spending to a balanced model (with margin focus in 2026) shows discipline. Overall, allocation prioritizes high-return areas like shelf-space gains and innovation.

The team has delivered strong top-line execution, though integration costs from acquisitions have been a near-term focus.

5. Financials, Growth Drivers & Customer Dynamics

Celsius has delivered impressive growth:

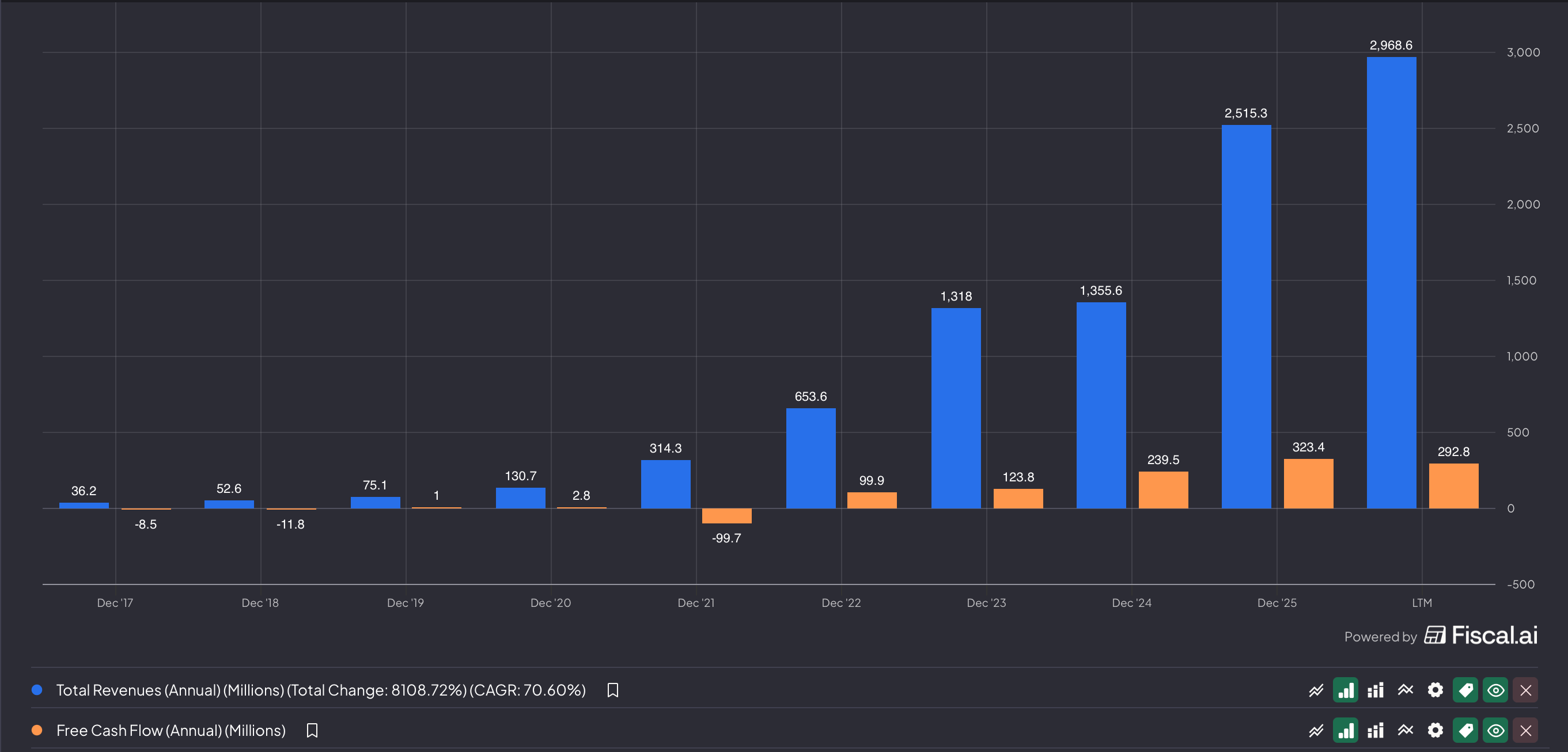

2025 revenue ~$2.5 billion (up ~85% YoY in some reports).

Operating Margin: Improved to 17.8% (up from 15.8% in Q1 2025)

Strong gross margins (near 50%) with operating leverage potential.

2026 expectations center on continued double-digit growth, shelf-space gains, and margin recovery.

Growth Drivers:

Shelf-space expansion and distribution improvements via PepsiCo.

Portfolio synergies and innovation (LTOs, new formats).

International market penetration.

Shift toward higher-margin premium offerings.

Customer dynamics are positive: broad retail presence (250k+ doors), high velocity in core channels, and appeal across fitness and wellness consumers. Revenue is diversified across brands and channels, with low concentration risk. Subscription or loyalty elements in some areas support recurring purchases.

6. Risks, Mitigants & Scenarios

Key Risks:

Competition: Red Bull, Monster, and private labels (e.g., Costco) fight for shelf space and share.

Integration & Execution: Merging acquired brands and optimizing PepsiCo distribution.

Input Costs: Volatility in aluminum, ingredients, and promotions.

Category Maturity: Slower growth if the U.S. energy drink boom moderates.

Valuation: Premium multiple leaves little room for disappointment.

Mitigants: Strong brand positioning, diversified portfolio, distribution scale, and innovation cadence.

Scenarios:

Bull: Accelerated shelf gains and international success drive 20–30%+ growth with margin expansion.

Base: Steady execution supports mid-teens growth and stable profitability.

Bear: Competitive pressure or cost inflation leads to slower growth and multiple compression.

7. Technical Analysis

After price hit an all-time high of nearly $100, a failed double top followed with a very sharp and steep correction; this is very typical wave 2 behavior. Price was able to find support at the 0.786 fib level and then ran over 200% in its intermediate 5 wave impulsive cycle. Since, we have been in an intermediate ABC correction which has currently found support at the 0.854 fib level. This is important to hold from a technical level, because it would mark the first major higher low since our wave 2 bottom. The structure of the weekly candlestick shows a long lower wick, which represents a lot of buyers bidding the price up. Overall, we like the structure price is giving us, and like the long-term potential returns forecasted.

Conclusion & Investment Summary

Celsius Holdings has built a strong position in the functional energy category with an expanding portfolio and powerful distribution. Its brand moat and innovation focus position it for continued share gains in a growing market.

CELH suits retail investors bullish on health & wellness trends who can tolerate CPG volatility. Combine this with your technical analysis for entry timing. This is educational only — do your own research.

Nice analysis, I stopped drinking them do to the artificial sweeteners